Business

Samsung Ordered to Pay $445.5 Million for Infringing Wireless Technology Patents

A federal jury in Marshall, Texas, has ordered Samsung Electronics to pay nearly $445.5 million in damages to Collision Communications after finding the tech giant guilty of infringing on multiple wireless communication patents.

The jury determined that Samsung’s Galaxy smartphones, laptops, and other wireless-enabled devices violated four patents owned by Collision Communications, which are related to 4G, 5G, and Wi-Fi communication standards.

This ruling adds to a series of multi-million-dollar patent infringement verdicts against Samsung in the same Texas court in recent years.

Collision Communications, based in Peterborough, New Hampshire, filed the lawsuit in 2023, alleging that Samsung used its patented technology—originally developed through research by defense contractor BAE Systems—to enhance wireless network efficiency. BAE Systems, however, is not involved in the case.

Samsung has denied the allegations, arguing that the patents in question are invalid. Representatives from both companies have yet to issue public comments following the verdict.

Source: Reuters

Business

Finance Minister Unveils 1,200MW Gas Power Project, Promises Cheaper Electricity and 3,000 Jobs

Finance Minister Dr. Cassiel Ato Forson has announced that the government is developing a 1,200-megawatt combined-cycle gas-powered plant at Kafodzidzi in the Komenda-Edina-Eguafo-Abrem (KEEA) Municipality.

Speaking during the midyear budget review in Parliament, the Finance Minister said visibility studies have confirmed the project’s viability, with environmental, engineering and permitting processes already completed.

According to him, the first 600MW phase of the project is expected to become operational in 2028, marking a major milestone in government’s efforts to boost electricity generation capacity.

Dr. Forson disclosed that to cut project costs, the government secured gas turbines directly from the manufacturer, GE Vernova, instead of using third-party procurement channels. He said the approach is expected to deliver cost savings of between 35% and 45%.

He added that once completed, the project will significantly reduce electricity generation costs, paving the way for a 10% to 20% reduction in electricity tariffs.

The Finance Minister also revealed that the first phase of the project is expected to create more than 3,000 direct and indirect jobs, providing a major boost to employment while strengthening Ghana’s energy security.

By Maurice Otoo

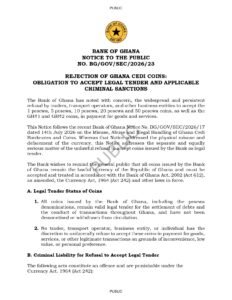

The Bank of Ghana (BoG) has issued a public notice warning traders, transport operators, businesses, and individuals that refusing to accept Ghana cedi coins as payment is unlawful and may attract criminal sanctions.

The notice, numbered BG/GOV/SEC/2026/23, addresses the growing practice of rejecting coins in commercial transactions across the country. According to the central bank, this behavior undermines the legal status of Ghana’s currency and violates existing laws.

Coins Remain Legal Tender

The Bank of Ghana stated that all coins it has issued—including 1 pesewa, 5 pesewa, 10 pesewa, 20 pesewa, 50 pesewa, GH¢1, and GH¢2 coins—remain valid legal tender throughout Ghana.

The central bank emphasized that none of these coins have been demonetized or withdrawn from circulation. Therefore, they must be accepted for the settlement of debts and payments for goods and services.

The notice follows an earlier BoG directive (Notice No. BG/GOV/SEC/2026/17), issued on July 14, 2026, which focused on the misuse, abuse, and illegal handling of Ghana cedi banknotes and coins. While the earlier notice dealt with physical damage and defacement of currency, the latest directive specifically addresses the unlawful refusal to accept coins.

Refusal to Accept Coins Is Illegal

The Bank made it clear that no trader, transport operator, business entity, or individual has the right to reject legal tender simply because the coins are considered inconvenient, of low value, or due to personal preference.

Businesses that refuse to sell goods or provide services because customers choose to pay with legal Ghana cedi coins may be committing an offence under the Currency Act, 1964 (Act 242).

Criminal Penalties

According to the notice, persons convicted of unlawfully refusing legal tender may face:

- Imprisonment for a term not exceeding three years;

- A fine;

- Or both imprisonment and a fine.

The Bank also warned that anyone who instructs, encourages, or assists another person to reject coins—for example, a business owner directing employees not to accept coins—may be held equally liable under the law.

Additionally, individuals caught committing the offence may be arrested without a warrant.

Enforcement Measures

The Bank of Ghana announced that it will collaborate closely with the Ghana Police Service and other law enforcement agencies to ensure compliance with the law.

The central bank warned that individuals and businesses that continue rejecting coins risk arrest, prosecution, fines, and possible imprisonment.

Members of the public experiencing difficulties with businesses refusing coins are encouraged to report such incidents to the nearest Bank of Ghana office, the Ghana Police Service, or through the Bank’s official communication channels.

Call to the Public

The Bank of Ghana urged all individuals, businesses, and institutions to support national efforts by accepting and responsibly handling Ghana’s currency in all its denominations.

The notice was signed by Aimee Vyda Quashie (Ms.), Secretary of the Bank, and is dated July 22, 2026.

Investor demand for Ghana’s Treasury bills surged last week, with the latest primary market auction attracting bids worth GH¢10.03 billion—almost double the government’s fundraising target of GH¢5.67 billion.

Results released by the Bank of Ghana show that the auction was oversubscribed by 77%, reflecting strong investor demand for short-term government securities and renewed confidence in the domestic debt market.

The Treasury accepted GH¢7.38 billion of the total bids, exceeding its financing target by GH¢1.71 billion after taking up a larger share of investor subscriptions.

The 364-day Treasury bill remained the most sought-after instrument, attracting GH¢5.65 billion in bids. The government accepted GH¢4.53 billion of that amount, making it the largest contributor to the funds raised during the auction.

The benchmark 91-day Treasury bill recorded bids of GH¢2.98 billion, with GH¢1.80 billion accepted, while the 182-day bill received GH¢1.40 billion in subscriptions, of which GH¢1.06 billion was accepted.

Yields were mixed across the three tenors. The 91-day bill eased slightly by one basis point to 5.86% from 5.87% at the previous auction, while the 182-day bill remained unchanged at 7.79%. The yield on the 364-day bill, however, climbed seven basis points to 12.99% from 12.92%, indicating continued investor preference for higher returns on longer-term government securities.

The latest auction represents a significant turnaround from the previous sale, which attracted just GH¢4.16 billion in bids. The sharp rise in subscriptions signals growing investor confidence in Treasury bills despite the prevailing interest rate environment.

Looking ahead, the government is targeting GH¢7.36 billion in its next Treasury bill sale under Tender 2016 to finance its short-term borrowing requirements.

‘She Was My Helper’ — Obaapa Christy Mourns Vivian Jill’s Late Sister Mabel Intuah

“I’m a better songwriter than AI”:Ras Kuuku

Many Ghanaian Musicians Are Going Broke Because They Rely on Streaming:Ras Kuuku

-

Entertainment2 weeks ago

Entertainment2 weeks agoDerrick Manny Calls for Better Support for Ghanaian Creatives Following Dede Padiki’s Death

-

Entertainment1 week ago

Entertainment1 week ago“Stay Broke If You Want Peace” – Sarkodie Sparks Online Debate With Powerful Success Message

-

General News2 weeks ago

General News2 weeks agoOkatakyie Afrifa Mensah’s Team Alleges Assault, Gunshot Injuries After Arrest

-

General News2 weeks ago

General News2 weeks agoEOCO Arrests Dennis Aboagye, Gerald Appiah Over GH¢55m IMCCoD Probe

-

Entertainment1 week ago

Dede Padiki Felt Neglected by Ghana’s Creative Sector Before Her Death – Derrick Manny

-

Entertainment2 weeks ago

Entertainment2 weeks agoMercy Asiedu donates GH¢50,000 to support Kwadwo Kwakye Obuobi’s kidney transplant

-

Business2 weeks ago

Business2 weeks agoInvestor Confidence Soars as Treasury Bill Bids Hit GH¢10.03 Billion

-

Entertainment3 days ago

Entertainment3 days agoDJ K.A Apologises Over Viral Video, Says It Was Recorded Four Years Ago