Business

Ghana beats IMF reserve target ahead of schedule

Ghana has surpassed a key milestone under its IMF programme—more than a year ahead of schedule.

According to a recent update following a staff-level agreement between the government and the International Monetary Fund, Ghana’s gross international reserves have already exceeded the target set for May 2026.

Fresh data from the Bank of Ghana shows that as of February 2025, the country’s gross international reserves stood at $9.3 billion—equivalent to four months of import cover.

Under the IMF programme, Ghana was expected to reach this threshold by mid-2026.

This early achievement is seen as a major boost to investor confidence and could bolster the stability of the Cedi in the coming months.

Analysts say unless the economy is hit by any major external shocks, Ghana is well-positioned to exit the IMF programme with stronger reserve buffers.

The anticipated disbursement of $370 million from the IMF in June 2025 is also expected to further support the central bank’s efforts to sustain macroeconomic stability.

Market watchers maintain that the Bank of Ghana should continue refining its liquidity-tightening tools while ensuring proactive monitoring of foreign exchange markets to prevent excessive speculation.

Adding that enhanced coordination between fiscal and monetary policies will help anchor inflation expectations and stabilize the Cedi.

Source: Citi Newsroom

Ghana economic recovery has made meaningful progress following the country’s recent macroeconomic challenges, but the gains remain fragile and should not be viewed as a permanent turnaround, according to audit and advisory firm PwC.

In its review of the 2026 Mid-Year Budget, presented by Finance Minister Dr. Cassiel Ato Forson, PwC acknowledged that Ghana has achieved notable improvements in key macroeconomic indicators during the first half of 2026. However, the firm cautioned that maintaining the recovery will require continued fiscal discipline, structural reforms, and resilience against increasing global economic risks.

According to PwC, the Finance Minister was justified in highlighting the country’s stronger economic performance compared to the same period last year.

“The Minister for Finance is right to argue that macroeconomic conditions in the first half (H1) of 2026 were significantly better than a year earlier,” the firm stated.

However, PwC stressed that the critical issue is whether these improvements are sustainable enough to attract long-term investment.

“The more important question for everybody, including business leaders, is whether the improvement is structural, durable and investable.”

Improved Indicators Signal Recovery

PwC noted that several economic indicators have recorded significant improvements, including:

* Higher economic growth

* Lower inflation compared to previous years

* Stronger fiscal balances

* Improved foreign exchange reserves

* Better debt sustainability indicators

The firm explained that some of these gains are the result of prudent fiscal management and progress made under Ghana’s debt restructuring programme.

However, it also pointed out that other positive developments have been supported by temporary factors such as:

* Favourable statistical base effects

* Delayed government expenditure

* Lower domestic interest rates

* Improved foreign reserve accumulation

PwC warned that these supportive conditions may become more difficult to sustain during the second half of 2026 as government increases spending on capital projects, inflationary pressures rise, and external economic uncertainties persist.

Inflation Risks Remain

While PwC believes the government’s year-end targets for real GDP growth and primary surplus remain achievable, it expressed concern over inflation.

The firm warned that recent increases in inflation, coupled with rising global crude oil prices and escalating geopolitical tensions, could push inflation towards the upper end of the government’s target range before the end of the year.

Businesses Urged to Remain Cautious

PwC advised businesses and investors not to assume that the current macroeconomic stability will continue without challenges.

“For business leaders and investors, our message is straightforward: Ghana’s macro picture is much improved, but this is not yet a no-risk operating environment.”

The report predicts that the second half of 2026 is likely to be characterised by:

* Mild reflation

* Selective acceleration in government spending

* Continued external economic vulnerabilities

* Less room for additional monetary policy easing than markets currently anticipate

Fiscal Strategy Viewed as Credible

PwC described the government’s fiscal strategy as broadly credible, noting that the administration has maintained its original revenue and expenditure projections without introducing a supplementary budget or significantly relaxing fiscal policy.

Nonetheless, the firm said long-term fiscal sustainability will depend on several critical reforms, including:

* Strengthening domestic revenue mobilisation

* Improving governance of state-owned enterprises

* Resolving persistent financial challenges within Ghana’s energy sector

PwC concluded that although Ghana’s fiscal position has improved, it cannot yet be considered fully repaired.

“Our independent judgment is that fiscal sustainability is improving, but it is not conclusively repaired.”

The report added that part of the stronger fiscal performance recorded during the first half of 2026 may have resulted from delayed government spending rather than permanent improvements in expenditure efficiency.

“Part of the fiscal strength reflects opportune timing rather than permanent efficiency.”

According to the firm, fiscal savings achieved earlier in the year could narrow as government ramps up spending on flagship programmes during the remainder of 2026.

Outlook Remains Positive but Requires Discipline

Despite the risks, PwC believes Ghana’s current macroeconomic environment offers better opportunities for businesses than in recent years.

Lower interest rates, stronger investor confidence and improved exchange-rate stability are expected to support investment and economic activity.

However, the firm urged businesses to adopt what it described as “disciplined optimism” by taking advantage of improving conditions while continuing to hedge against currency volatility, safeguard profit margins and prepare for a potentially more challenging second half of the year.

PwC’s assessment suggests that while Ghana economic recovery is gaining momentum, sustaining the progress will require consistent policy implementation, continued fiscal discipline and successful structural reforms to withstand both domestic and global economic pressures.

Business

BoG Lost Its Independence Under NPP, Leading to Debt Exchange Crisis – Banking Consultant Alleges

A Banking Consultant, Dr. Richmond Atuahene, has argued that the independence of the Bank of Ghana (BoG) is essential to protecting the country’s financial system from political interference, claiming that government influence over the central bank contributed significantly to Ghana’s recent economic challenges.

In a zoom interview granted on Kessben TV’s Digest show, Dr. Atuahene insisted, the Bank of Ghana should operate independently without interference from any government, stressing that central bank autonomy is a globally accepted principle designed to safeguard sound monetary policy.

He alleged that the previous NPP administration dictated the operations of the central bank, a situation he believes ultimately resulted in the Domestic Debt Exchange Programme (DDEP).

“The Bank of Ghana should operate as an independent entity devoid of political interference, but the NPP government dictated its mode of operation, and that led to the Domestic Debt Exchange Programme,” he stated.

Dr. Atuahene further claimed that the debt exchange became necessary because the central bank had extended substantial financing to the government, weakening its financial position.

He also criticized the currency redenomination exercise, asserting that it was a government-driven policy rather than an independent decision by the Bank of Ghana.”The redenomination was Kufuor’s policy and not Dr. Paul Acquah’s own. It was pure government interference, not Central Bank policy,” he claimed.

The banking consultant warned that Ghana currently lacks the resources needed to fully recapitalize the Bank of Ghana, suggesting that the country’s financial system may continue to feel the effects of the central bank’s losses for several more years unless decisive measures are taken.

Dr. Atuahene maintained that preserving the independence of the Bank of Ghana is critical to preventing future economic crises and restoring confidence in the country’s financial sector.

By Maurice Otoo

Business

Finance Minister Unveils 1,200MW Gas Power Project, Promises Cheaper Electricity and 3,000 Jobs

Finance Minister Dr. Cassiel Ato Forson has announced that the government is developing a 1,200-megawatt combined-cycle gas-powered plant at Kafodzidzi in the Komenda-Edina-Eguafo-Abrem (KEEA) Municipality.

Speaking during the midyear budget review in Parliament, the Finance Minister said visibility studies have confirmed the project’s viability, with environmental, engineering and permitting processes already completed.

According to him, the first 600MW phase of the project is expected to become operational in 2028, marking a major milestone in government’s efforts to boost electricity generation capacity.

Dr. Forson disclosed that to cut project costs, the government secured gas turbines directly from the manufacturer, GE Vernova, instead of using third-party procurement channels. He said the approach is expected to deliver cost savings of between 35% and 45%.

He added that once completed, the project will significantly reduce electricity generation costs, paving the way for a 10% to 20% reduction in electricity tariffs.

The Finance Minister also revealed that the first phase of the project is expected to create more than 3,000 direct and indirect jobs, providing a major boost to employment while strengthening Ghana’s energy security.

By Maurice Otoo

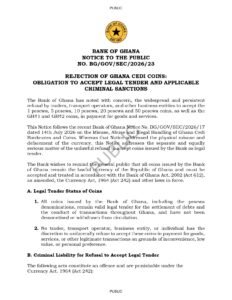

The Bank of Ghana (BoG) has issued a public notice warning traders, transport operators, businesses, and individuals that refusing to accept Ghana cedi coins as payment is unlawful and may attract criminal sanctions.

The notice, numbered BG/GOV/SEC/2026/23, addresses the growing practice of rejecting coins in commercial transactions across the country. According to the central bank, this behavior undermines the legal status of Ghana’s currency and violates existing laws.

Coins Remain Legal Tender

The Bank of Ghana stated that all coins it has issued—including 1 pesewa, 5 pesewa, 10 pesewa, 20 pesewa, 50 pesewa, GH¢1, and GH¢2 coins—remain valid legal tender throughout Ghana.

The central bank emphasized that none of these coins have been demonetized or withdrawn from circulation. Therefore, they must be accepted for the settlement of debts and payments for goods and services.

The notice follows an earlier BoG directive (Notice No. BG/GOV/SEC/2026/17), issued on July 14, 2026, which focused on the misuse, abuse, and illegal handling of Ghana cedi banknotes and coins. While the earlier notice dealt with physical damage and defacement of currency, the latest directive specifically addresses the unlawful refusal to accept coins.

Refusal to Accept Coins Is Illegal

The Bank made it clear that no trader, transport operator, business entity, or individual has the right to reject legal tender simply because the coins are considered inconvenient, of low value, or due to personal preference.

Businesses that refuse to sell goods or provide services because customers choose to pay with legal Ghana cedi coins may be committing an offence under the Currency Act, 1964 (Act 242).

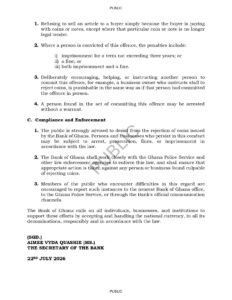

Criminal Penalties

According to the notice, persons convicted of unlawfully refusing legal tender may face:

- Imprisonment for a term not exceeding three years;

- A fine;

- Or both imprisonment and a fine.

The Bank also warned that anyone who instructs, encourages, or assists another person to reject coins—for example, a business owner directing employees not to accept coins—may be held equally liable under the law.

Additionally, individuals caught committing the offence may be arrested without a warrant.

Enforcement Measures

The Bank of Ghana announced that it will collaborate closely with the Ghana Police Service and other law enforcement agencies to ensure compliance with the law.

The central bank warned that individuals and businesses that continue rejecting coins risk arrest, prosecution, fines, and possible imprisonment.

Members of the public experiencing difficulties with businesses refusing coins are encouraged to report such incidents to the nearest Bank of Ghana office, the Ghana Police Service, or through the Bank’s official communication channels.

Call to the Public

The Bank of Ghana urged all individuals, businesses, and institutions to support national efforts by accepting and responsibly handling Ghana’s currency in all its denominations.

The notice was signed by Aimee Vyda Quashie (Ms.), Secretary of the Bank, and is dated July 22, 2026.

Investor demand for Ghana’s Treasury bills surged last week, with the latest primary market auction attracting bids worth GH¢10.03 billion—almost double the government’s fundraising target of GH¢5.67 billion.

Results released by the Bank of Ghana show that the auction was oversubscribed by 77%, reflecting strong investor demand for short-term government securities and renewed confidence in the domestic debt market.

The Treasury accepted GH¢7.38 billion of the total bids, exceeding its financing target by GH¢1.71 billion after taking up a larger share of investor subscriptions.

The 364-day Treasury bill remained the most sought-after instrument, attracting GH¢5.65 billion in bids. The government accepted GH¢4.53 billion of that amount, making it the largest contributor to the funds raised during the auction.

The benchmark 91-day Treasury bill recorded bids of GH¢2.98 billion, with GH¢1.80 billion accepted, while the 182-day bill received GH¢1.40 billion in subscriptions, of which GH¢1.06 billion was accepted.

Yields were mixed across the three tenors. The 91-day bill eased slightly by one basis point to 5.86% from 5.87% at the previous auction, while the 182-day bill remained unchanged at 7.79%. The yield on the 364-day bill, however, climbed seven basis points to 12.99% from 12.92%, indicating continued investor preference for higher returns on longer-term government securities.

The latest auction represents a significant turnaround from the previous sale, which attracted just GH¢4.16 billion in bids. The sharp rise in subscriptions signals growing investor confidence in Treasury bills despite the prevailing interest rate environment.

Looking ahead, the government is targeting GH¢7.36 billion in its next Treasury bill sale under Tender 2016 to finance its short-term borrowing requirements.

2026 BECE Results Out; WAEC Takes Firm Action Against Examination Malpractice

VALCO Strategic Equity Capitalization: Minority Backs Workers, Demands Full Transparency

Supreme Court: OSP Can Probe Corruption but Cannot Independently Prosecute Without Attorney-General’s Authority

-

Entertainment1 week ago

Entertainment1 week agoDJ K.A Apologises Over Viral Video, Says It Was Recorded Four Years Ago

-

General News1 week ago

General News1 week agoDr. Charles Dwamena Sues Hubtel for GH¢5 Million Over Alleged Campaign USSD Sabotage

-

General News2 weeks ago

General News2 weeks agoOkatakyie Afrifa Granted GH¢100,000 Bail Over Alleged Disruption of NPP Constituency Elections

-

Entertainment2 weeks ago

Entertainment2 weeks agoGhanaians Question Akwaboah’s Advice to Save GH¢8,000 Monthly Before Marriage

-

General News1 week ago

General News1 week agoChairman Wontumi Sentenced to 20 Years in Prison Over Illegal Mining

-

Entertainment3 days ago

Entertainment3 days agoGhana Secures $3.5 Million UNESCO Heritage Support During Tourism Minister’s South Korea Visit

-

Entertainment1 week ago

Entertainment1 week ago“Hits Rule Everything Now” — Perez Musik Says Legends Like Bob Marley Would Face Challenges Today

-

Entertainment1 week ago

Entertainment1 week agoRamatu Gumah Named Chairperson and Head of Africa Diaspora Relations at Africa Development Council